Weighted average anti-dilution is a widely used mechanism designed to balance investor protections with fairness to founders during a down-round. By factoring in the size and price of new share issuances relative to existing capital, this approach adjusts investors’ positions in a more equitable way compared to full ratchet protections.

Below we outline the key formulae behind weighted average anti-dilution. Whether applied via bonus issues or conversion adjustments, these calculations ensure clarity in maintaining economic balance across all stakeholders.

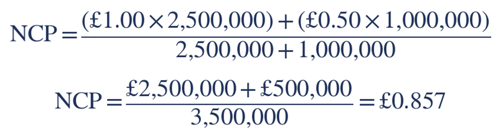

Series A investors purchased 1,000,000 shares at £1.00 per share.

The company issues 1,000,000 new shares at £0.50 per share.

Immediately before the new issue, the company has 2,500,000 shares in issue on a fully-diluted basis (the 1,000,000 Series A shares together with 1,500,000 founder and option-pool shares).

Using the broad-based weighted average formula:

Where:

SIP = Starting Price (the issue/conversion price of the original Equity Share, £1.00 in this case)

QISP = Weighted average equivalent price per Equity Share in respect of the new Equity Shares issued (in this case, £0.50).

ESC = the number of Equity Shares in issue

NS = The number of new Equity Shares issued (1,000,000).

In this case:

The conversion price is adjusted to £0.857, increasing the number of ordinary shares the investor receives upon conversion.

In a similar scenario, a bonus issue would adjust the investor’s position as follows:

Using the broad-based weighted average formula:

Where:

N = The number of Anti-Dilution Shares to be issued to the Exercising Investor

WA =

SIP = Starting Price (the issue price of the original shares, £1.00 in this case)

ESC = the number of Equity Shares in issue

QISP = Weighted average equivalent price per Equity Share in respect of the new Equity Share issued (in this case, £0.50).

NS = The number of new Equity Shares issued (1,000,000).

Z = The number of Series A Shares held by the Exercising Investor immediately prior to issue (1,000,000).

Using the broad-based weighted average formula:

Substituting values:

ESC = 1,000,000 (Number of Equity Shares before issue)

SIP = £1.00

NS = 1,000,000 (New Equity Shares Issued)

QISP=0.50 (Issue Price of New Equity Shares)

Using the formula:

Substitute:

SIP = £1.00

WA = £0.857

Z = 1,000,000

The Series A investors will receive an additional 167,000 shares to preserve their economic position relative to the new valuation and, as a result hold 1,167,000 shares following the bonus issue.

Find out more about anti-dilution protections in this article from our 'Anatomy of a term sheet' series.

Our 'Anatomy of a term sheet' series breaks down each critical section of a venture capital term sheet, offering technical insights and practical real-world examples to help founders with their fundraising journey.

Our aim is to demystify term sheets and empower founders and their advisors to navigate negotiations with clarity and confidence.

Anatomy of a Term Sheet Overview Discover our work in venture & growth capital

Chris Dyson

Partner and Head of Technology Sector

+44 (0)117 321 8054 c.dyson@ashfords.co.uk View more

Rory Suggett

Partner and Head of Corporate

+44 (0)117 321 8067 +44 (0)7912 270526 r.suggett@ashfords.co.uk View more

Jocelyn Ormond

Partner and Head of the Healthcare & Life Sciences Sector

+44 (0)7872677082 j.ormond@ashfords.co.uk View more

Andrew Betteridge

Partner and Head of Business & Wealth Division

+44 (0)117 321 8063 +44 (0)7843 265362 a.betteridge@ashfords.co.uk View moreWe produce a range of insights and publications to help keep our clients up-to-date with legal and sector developments.

Sign up